A family office is defined as a private operating model that manages the entire financial ecosystem of an ultra-high-net-worth family, covering everything from entity accounting and governance to lifestyle administration. A wealth manager, by contrast, is an investment and financial planning advisor who serves affluent individuals with less complex needs. The distinction between a family office vs wealth manager is not simply one of scale. It is a difference in structure, scope, and purpose. Knowing which model fits your situation is one of the most consequential financial decisions you will make.

What services do family offices provide compared to wealth managers?

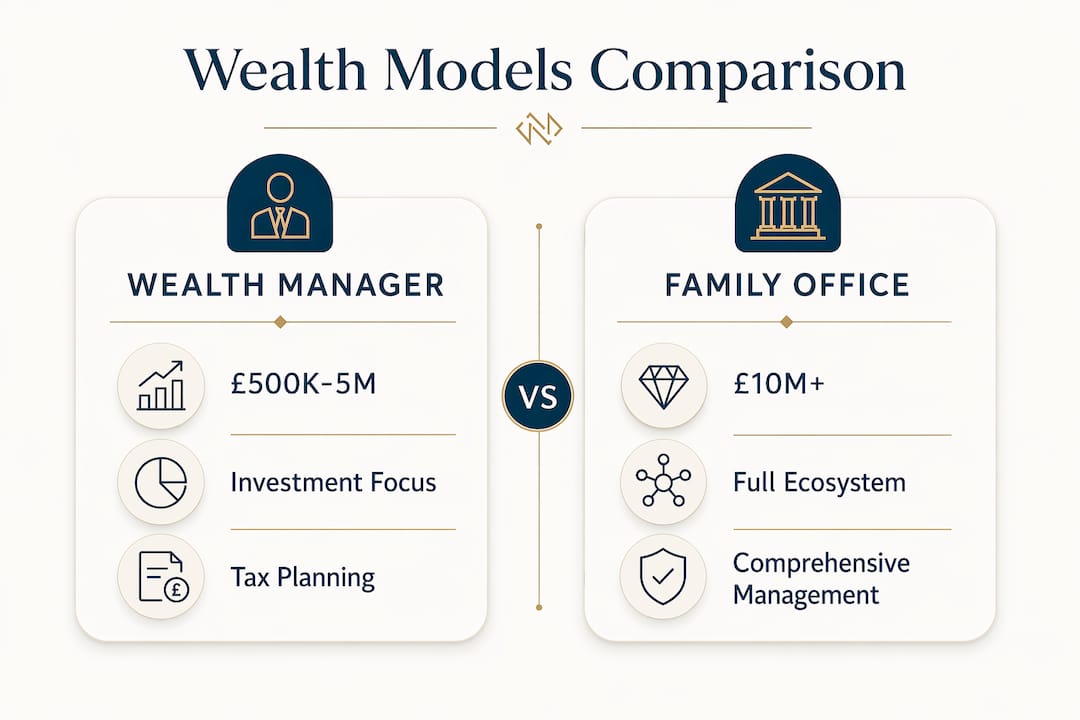

Wealth managers focus on investment portfolios, retirement planning, and tax strategy. They are advisors. They give guidance and execute within a defined financial brief. That is genuinely valuable for the right client at the right stage of wealth.

A family office operates at a fundamentally different level. Family offices manage full financial ecosystems beyond advice, handling entity-level accounting, bill payment, cash controls, consolidated reporting across trusts and other legal structures, vendor coordination, and multi-generational governance. The family office does not just advise. It runs things.

The practical difference shows up in day-to-day operations. A wealth manager will review your portfolio quarterly and flag tax exposure. A family office will manage the payroll for your household staff, coordinate your aviation schedule, oversee your insurance renewals, and report across every trust and entity you hold, all under one roof. Family office services extend into lifestyle and governance in ways that no traditional wealth management firm is structured to replicate.

Bespoke family office offerings can include:

- Multi-generational wealth governance and family constitution drafting

- Household and property administration

- Aviation and travel management

- Art, watch, and collectible asset oversight

- Consolidated reporting across multiple legal entities

- Concierge and lifestyle services, including access to rare events

Pro Tip: If you find yourself coordinating more than three separate advisors across tax, legal, investment, and lifestyle, that coordination burden alone is a signal that a family office structure may serve you better.

At what wealth level should families consider a family office?

The wealth thresholds that define each model are well established. Wealth managers typically serve clients with £500,000 to £5 million in assets. Multi-family offices become appropriate at £10–25 million. Single-family offices below £50–100 million are rarely viable. These are not arbitrary numbers. They reflect the cost of running each structure against the benefit it delivers.

| Wealth level | Appropriate model | Primary rationale |

|---|---|---|

| £500,000 to £5 million | Wealth manager | Investment and tax planning sufficient for complexity at this level |

| £10 million to £25 million | Multi-family office | Shared infrastructure reduces cost while expanding service scope |

| £50 million to £100 million+ | Single-family office | Dedicated structure justifiable given asset complexity and privacy needs |

Wealth thresholds alone do not tell the full story. Complexity is an equally important trigger. Families with international assets, multiple business entities, cross-border residency, or significant illiquid holdings often need family office coordination well before they reach the single-family office threshold. Multi-generational wealth governance frequently triggers the transition, particularly when a family needs independent structures beyond individual decision-making.

The right question is not only “how much do we have?” but “how complex has this become?” A family managing a single investment portfolio has different needs from one overseeing a property portfolio, a trading business, offshore trusts, and a philanthropic foundation simultaneously.

Pro Tip: If your accountant, solicitor, investment manager, and insurance broker have never spoken to each other, you are already operating without the coordination that a family office provides. That gap has a cost, even if it is invisible.

How do cost structures and fee models differ?

Cost is where the family office vs private wealth manager comparison becomes most concrete. Wealth managers charge annual fees based on assets under management, typically in the range of 0.5% to 1.5%. On a £2 million portfolio, that is £10,000 to £30,000 per year. The model is straightforward and the cost scales with your assets.

Family offices carry a very different cost profile. Establishing a single-family office may cost tens of millions due to dedicated staff and infrastructure. That includes hiring a chief investment officer, a family office director, legal counsel, accountants, and administrative staff, all employed exclusively for one family. The ongoing annual cost is substantial.

Multi-family offices offer a middle path. Multi-family offices reduce operational costs by 30–50% compared to single-family offices, with family office services typically costing £500,000 to £2 million annually depending on scope. That cost is shared across multiple families, which makes the model accessible to families in the £10–25 million range who want family office depth without single-family office expense.

The value calculation goes beyond fees. A family office delivers privacy, control, and coordination that no percentage-based advisory fee can replicate. For families with genuinely complex structures, the cost of not having that coordination, measured in tax inefficiency, missed governance, and uncoordinated advisors, frequently exceeds the cost of the office itself.

- Wealth manager fees: 0.5%–1.5% of assets under management annually

- Multi-family office annual costs: £500,000 to £2 million, shared across families

- Single-family office: tens of millions in setup and ongoing operational costs

- Hidden cost of poor coordination: tax leakage, governance gaps, and duplicated effort across advisors

Can families use both a wealth manager and a family office?

The short answer is yes, and many do. A family office is an operating model, not a replacement for every external advisor. Family offices and wealth advisory firms are not mutually exclusive. Many ultra-wealthy families retain external investment managers while the family office handles governance, administration, and consolidated oversight.

The family office acts as the coordinator. It sets the brief, monitors performance, and holds external advisors accountable. The wealth manager executes within that brief. This structure gives families the best of both: specialist investment expertise from the market, and independent oversight from the family office.

A practical collaboration model works as follows:

- The family office defines the investment policy statement and risk parameters.

- External wealth managers or specialist fund managers execute within those parameters.

- The family office consolidates reporting across all managers and entities.

- The family office reviews advisor performance independently, free from conflicts of interest.

- Governance decisions, including succession and philanthropy, remain within the family office structure.

Some families who are not yet ready for a full family office use wealth advisory platforms that replicate family office functions. These platforms offer consolidated reporting, multi-advisor coordination, and governance support without the cost of a dedicated internal structure. NXD Family Office operates on a similar principle: providing the coordination, independence, and breadth of a family office without requiring clients to build one from scratch.

What factors beyond wealth size influence the decision?

Wealth size sets the threshold. Other factors determine the timing and the model. Families considering the difference between a family office and a wealth manager should weigh the following:

- Privacy. A family office keeps sensitive financial information within a dedicated, trusted team. Wealth management firms serve many clients and operate within broader institutional structures.

- Asset complexity. International property, aviation assets, art collections, and multi-entity business structures all demand coordination that a single wealth manager cannot provide.

- Family dynamics. Multi-generational families with differing risk appetites, competing interests, and succession considerations need governance structures, not just investment advice.

- Control. Families who want direct oversight of every financial decision benefit from the family office model. Those who prefer to delegate fully may find a wealth manager sufficient.

- Lifestyle needs. Bespoke lifestyle services, from event access to concierge support, sit naturally within a family office but outside the scope of any wealth management firm.

The preference for control versus delegation is often the deciding factor. Independent advisors who operate without referral fees or commission incentives are the foundation of any trustworthy family office model. Without that independence, the structure exists in name only.

Key takeaways

A family office is the right structure when wealth complexity outgrows what any single advisor or wealth management firm can coordinate effectively.

| Point | Details |

|---|---|

| Scope defines the difference | Wealth managers advise on investments and tax; family offices run the full financial operation. |

| Wealth thresholds matter | Wealth managers suit £500k–£5m; multi-family offices suit £10m–£25m; single-family offices suit £50m+. |

| Cost scales with structure | Multi-family offices cost £500k–£2m annually; single-family offices can cost tens of millions to establish. |

| Both models can coexist | Family offices coordinate external wealth managers rather than replacing them. |

| Complexity triggers the transition | International assets, multi-entity structures, and multi-generational governance signal the need for a family office. |

Why the timing of this decision matters more than most families realise

Alex Goldstein here. I have watched families delay the transition from wealth manager to family office for years, often because the cost feels prohibitive or the need feels abstract. The moment it becomes concrete is usually a crisis: a tax inefficiency that cost seven figures, a governance dispute between siblings, or an advisor conflict of interest that nobody caught because nobody was watching.

The families who get this right do not wait for a crisis. They recognise that wealth, beyond a certain level, stops being a portfolio and becomes a system. Systems need management, not just advice. The difference between family wealth advisors who genuinely serve your interests and those who serve their own is not always visible until it is too late.

My honest view is that the multi-family office model is underused by families in the £10–25 million range. They assume a family office is out of reach financially, so they stay with a wealth manager who cannot provide the coordination they actually need. The cost of that gap, in missed tax efficiency, uncoordinated advisors, and governance drift, frequently exceeds the cost of the right structure. Assess the breadth of what you need first. Then work backwards to the cost.

— Alex Goldstein

How NXD Family Office supports high-net-worth families

NXD Family Office provides the coordination, independence, and breadth of a family office without the overhead of building one internally. Every client receives unbiased advice, free from referral fees or commissions, across financial planning, insurance, lifestyle assets, and concierge services.

Whether you are weighing up wealth management services for the first time or considering whether your current structure still fits your complexity, NXD Family Office offers the expert guidance to make that call clearly. From asset watches and aviation to rare event access and multi-generational governance, the team handles what most advisors cannot. If you are ready to explore what a genuinely independent family office model looks like for your family, the conversation starts here.

FAQ

What is the main difference between a family office and a wealth manager?

A wealth manager advises on investments, tax, and retirement planning. A family office is a full operating model that manages entity accounting, governance, lifestyle administration, and multi-advisor coordination across an entire family’s financial structure.

At what net worth should I consider a family office?

Multi-family offices become appropriate at around £10–25 million in assets, while single-family offices are rarely viable below £50–100 million. Complexity of assets and family structure can trigger the need earlier.

How much does a family office cost compared to a wealth manager?

Wealth managers charge 0.5%–1.5% of assets under management annually. Family office services cost £500,000 to £2 million per year for multi-family offices, with single-family offices requiring tens of millions to establish.

Can I keep my wealth manager if I set up a family office?

Yes. Family offices typically coordinate external wealth managers rather than replace them. The family office sets the investment policy and monitors performance; the wealth manager executes within that framework.

What qualitative factors should influence my choice?

Privacy requirements, asset complexity, family governance needs, and the desire for independent oversight all influence the decision. Families with international assets, multiple entities, or multi-generational succession needs generally benefit from a family office structure sooner than wealth thresholds alone suggest.