TL;DR:

- A family office is a private organization dedicated to managing the wealth and personal affairs of an ultra-high-net-worth family. It offers comprehensive services, including investment management, estate planning, philanthropy, and lifestyle management, tailored to a family’s specific needs. Effective governance and succession planning are crucial for long-term wealth preservation, as many family offices lack formal structures in these areas.

A family office is a private organisation dedicated to managing the financial, investment, and personal affairs of an ultra-high-net-worth family. Unlike a private bank or wealth manager, it exists solely to serve one family or a small group of families, with no obligation to sell products or generate revenue from third parties. That distinction matters more than most people realise. The typical entry point sits at £40–80 million or more in investable assets, reflecting operational costs exceeding $1 million annually just to keep the lights on.

What is a family office and what does it actually do?

A family office is a private wealth management structure built around the specific needs of an ultra-high-net-worth family. The American Family Office Association and bodies such as the Family Office Association describe it as a dedicated entity covering everything from investment oversight to estate planning, tax strategy, and lifestyle management. Wikipedia defines it as a privately held company that handles investment management and wealth management for a wealthy family. The key word is private. There is no external shareholder to satisfy, no product quota to meet, and no commission driving the advice.

The scope goes well beyond picking stocks. A well-run family office coordinates legal counsel, philanthropic giving, succession planning, and even the management of household staff. That breadth is precisely why the structure is so powerful, and why it demands significant resources to operate properly.

Pro Tip: If you are evaluating whether a family office structure suits your situation, start by listing every financial and personal function your family currently outsources. If that list runs to ten or more distinct services, a coordinated office model will almost certainly save time and money.

What services does a family office provide?

Family office services explained span a far wider range than most families anticipate when they first encounter the concept. The core functions include:

- Investment management: Portfolio construction, asset allocation, manager selection, and performance reporting across public and private markets.

- Tax and legal advisory: Structuring assets to minimise liability, managing cross-border obligations, and coordinating with specialist solicitors.

- Estate and succession planning: Drafting wills, establishing trusts, and preparing the next generation to receive and steward wealth responsibly.

- Philanthropic coordination: Managing charitable foundations, donor-advised funds, and impact investment programmes.

- Family governance: Establishing family constitutions, holding family councils, and resolving disputes before they become costly.

- Concierge and lifestyle management: Securing rare experiences, managing property portfolios, overseeing aviation assets, and handling the kind of requests that simply cannot be delegated to a standard PA.

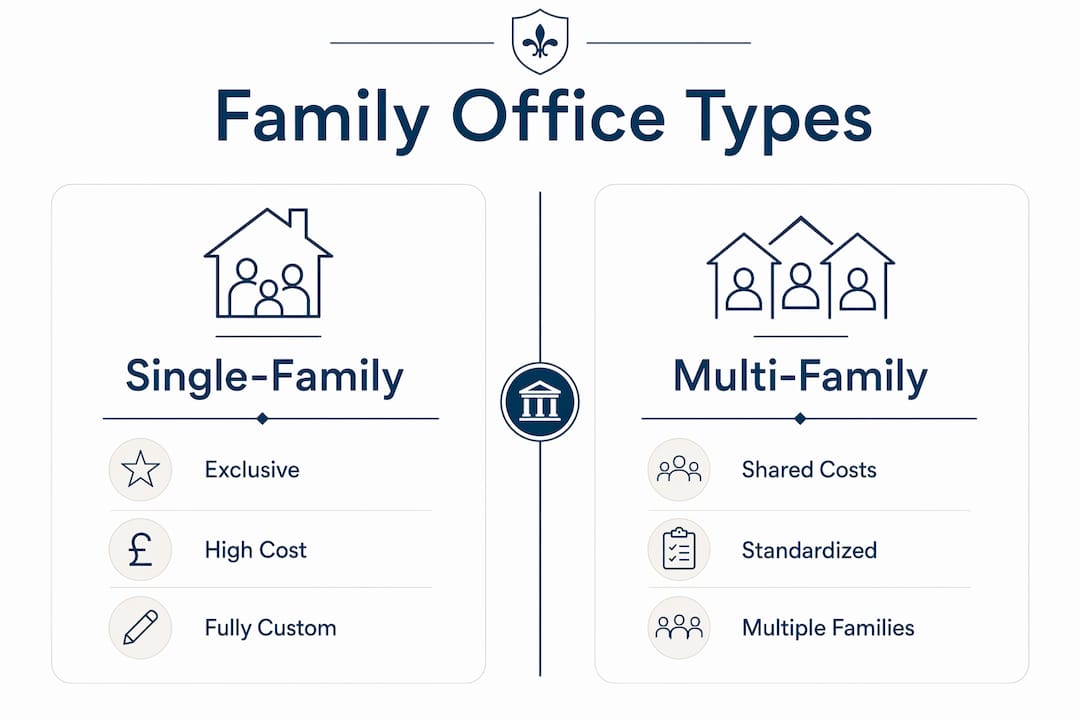

The difference between a single-family office and a multi-family office lies in how deeply these services are customised. A single-family office tailors every process to one family’s preferences, values, and risk appetite. A multi-family office spreads those capabilities across several client families, reducing cost per family while still delivering a high standard of service.

Pro Tip: Do not assume every family office offers the same depth in every category. Ask specifically which services are delivered in-house and which are outsourced. The answer tells you a great deal about where the real expertise sits.

What are the different types of family office?

Three main structures exist, and choosing the wrong one is an expensive mistake.

| Type | Who It Suits | Typical Cost | Key Trade-off |

|---|---|---|---|

| Single-family office | One family, $100M+ assets | $1M–$6.6M+ per year | Maximum control, highest cost |

| Multi-family office | Several families, $20M–$100M each | Shared operational costs | Less bespoke, broader network |

| Hybrid model | Families using private banking plus advisory | Variable, often lower | Convenience versus independence |

A single-family office is the most exclusive structure. Every member of staff works for one family, every system is built around one set of objectives, and every decision reflects one family’s values. That exclusivity carries a price. Billion-dollar-plus operations can cost $6.6 million or more annually to run. That figure covers staffing, technology, compliance, and governance, before a single investment is made.

A multi-family office shares those fixed costs across several client families. The trade-off is a degree of standardisation. Processes are built to serve a range of clients rather than one specific family, which means some bespoke elements are lost. For families with assets below $100 million, this model often delivers the best balance of sophistication and cost efficiency.

Hybrid models combine elements of private banking with family office advisory. They are common among families transitioning from a traditional banking relationship towards a more structured approach. The risk here is conflicts of interest. A bank-affiliated hybrid model may still carry product mandates that influence advice.

Pro Tip: When assessing a multi-family office, ask how many client families it currently serves and what the average asset level is. A firm serving 200 families at $20 million each operates very differently from one serving 15 families at $200 million each.

What does it cost to run a family office?

The cost question is where many families receive a rude awakening. Operational costs exceed $1 million annually for even a modest single-family office setup. That figure rises steeply with complexity. Families with assets above $1 billion typically spend $6.6 million or more each year on staffing, technology, legal compliance, and governance infrastructure alone.

The financial threshold for justifying a single-family office sits at $50–100 million in investable assets as a minimum. Below that level, the cost of running a dedicated office consumes a disproportionate share of returns. This is not a vanity threshold. It reflects the genuine overhead of employing qualified investment professionals, compliance officers, accountants, and legal advisors under one roof.

Non-financial costs are equally significant. Regulatory compliance, cybersecurity, and managing human dynamics across generations all demand time and expertise that money alone cannot buy. Governance failures, succession disputes, and data breaches have destroyed family wealth that survived multiple market cycles. Families should treat these risks with the same rigour they apply to investment decisions.

A common misconception is that a family office is primarily an investment vehicle. The reality is that wealth preservation and family governance are the true cornerstones of long-term success. Investment performance matters, but it is governance that determines whether wealth survives into the third and fourth generation.

How are family offices adapting investment strategies in 2026?

The global family office is shifting its investment posture decisively. Family offices are moving away from passive public equity exposure towards direct investing in real estate, private equity, and venture capital. This shift reflects both a search for higher returns and a desire for greater control over underlying assets.

The geographic picture is changing too. North America’s share of new family offices fell to 49% in 2025, down from 68% in 2024. Europe now accounts for 27% and Asia for 13%. This redistribution signals that the global family office model is no longer a North American story. Families in the UK, Singapore, and the UAE are establishing structures at a pace that reflects both wealth creation and regulatory maturity in those markets.

Economic and geopolitical uncertainty is driving strategic rethinking at pace. 60% of family offices plan to change their strategic asset allocation within the next 12 months. That is not a marginal adjustment. It represents a fundamental reassessment of risk, return, and resilience across the sector.

Key investment themes emerging from family office research in 2026 include:

- Private credit: Filling the gap left by retreating banks in mid-market lending.

- Direct real estate: Moving away from listed REITs towards direct property ownership.

- Venture capital: Earlier-stage commitments in technology, healthcare, and climate.

- Infrastructure: Long-duration assets that match multigenerational investment horizons.

Pro Tip: Align your investment strategy with your family’s generational timeline, not just a standard five-year horizon. A family office managing wealth for a 30-year-old founder and their children should hold a very different portfolio to one managing assets for a 70-year-old patriarch approaching estate transfer.

What governance and succession challenges do family offices face?

Governance is the area where family offices most frequently fall short, and the consequences are severe. Only 35% of family offices have a formal succession plan in place as of mid-2026. That statistic means the majority of family wealth structures have no documented answer to the question of what happens next.

The steps that distinguish well-governed family offices from poorly run ones are consistent:

- Establish a family constitution. Document values, decision-making authority, and conflict resolution processes before a dispute arises.

- Create a formal investment policy statement. Define risk tolerance, asset allocation boundaries, and prohibited investments in writing.

- Appoint an independent advisory board. External voices reduce the risk of groupthink and provide accountability.

- Run regular family education programmes. Next-generation members who understand the structure are far less likely to dismantle it.

- Review fiduciary independence annually. Confirm that advisors are operating in the family’s interest, not their own.

“Family offices are no longer primarily about investment returns. Resilience and governance are essential to managing generational legacy.” — Family Office Association

Conflicts of interest are a persistent risk. Some family offices operate with proprietary product mandates or incentivised fee structures that quietly redirect value away from the family. Families should verify fiduciary independence rigorously before committing to any operating model. The question to ask is direct: does this office earn more money when it recommends a particular product? If the answer is yes, or if the answer is unclear, that is a problem.

Key takeaways

A family office is the most comprehensive private wealth structure available, but its value depends entirely on governance, not just investment performance.

| Point | Details |

|---|---|

| Asset threshold matters | A minimum of $50–100 million in investable assets is required to justify a single-family office structure. |

| Services go beyond investment | Family offices cover tax, legal, estate planning, philanthropy, governance, and lifestyle management. |

| Governance is the weak point | Only 35% of family offices have a formal succession plan, leaving most wealth structures exposed. |

| Global diversification is accelerating | North America’s share of new family offices fell to 49% in 2025 as Europe and Asia expand rapidly. |

| Fiduciary independence is non-negotiable | Always verify whether your family office earns fees or commissions from the products it recommends. |

Why governance matters more than returns

I have spent years observing how families approach the decision to establish or join a family office structure. The pattern that concerns me most is the focus on investment performance at the expense of everything else. Families spend months selecting fund managers and debating asset allocation, then sign governance documents they have barely read.

The families who preserve wealth across generations are not necessarily the ones with the best investment returns. They are the ones who built clear decision-making structures, educated their children about the responsibilities of wealth, and chose advisors who had no financial incentive to steer them wrong. That last point is where the traditional advisory industry has consistently let families down. Too many advisors have their hand in the clients’ till through referral fees, product commissions, and opaque fee arrangements.

The rise of hybrid and multi-family office models is a direct response to this problem. Many families have found that a dedicated private office is not immediately necessary. A well-structured multi-family model, with genuine fiduciary independence, often delivers more value than a costly single-family setup with compromised advice. The key is knowing what questions to ask before you commit.

Regulatory and technological complexity will only increase through 2026 and beyond. Families that treat their office as a living institution, one that evolves with the regulatory environment and the needs of each generation, will be the ones still intact in 50 years.

— Alex Goldstein

How Nxdfamilyoffice can support your wealth and lifestyle

Nxdfamilyoffice was built specifically for families who are tired of advisors who prioritise their own revenue over client outcomes. The model is straightforward: no referral fees, no commissions, no hidden incentives. Every recommendation reflects what is genuinely best for the client.

From wealth management services and tax advisory through to private banking and lifestyle assets advisory, Nxdfamilyoffice coordinates every aspect of a family’s financial and personal life under one trusted relationship. Whether you are structuring family office relationships for the first time or reviewing an existing arrangement, the team at Nxdfamilyoffice brings the kind of bespoke expertise that simply does not exist in a standard wealth management firm. Consider it done.

FAQ

What is a family office in simple terms?

A family office is a private organisation that manages the wealth, investments, and personal affairs of an ultra-high-net-worth family. It acts as a dedicated team serving one family’s interests across finance, legal, lifestyle, and legacy planning.

How much money do you need to set up a family office?

The generally accepted minimum is $50–100 million in investable assets, as operational costs exceed $1 million annually for even a basic single-family structure. Families below this threshold typically find a multi-family office more cost-effective.

What is the difference between a single-family and multi-family office?

A single-family office serves one family exclusively, offering maximum customisation at the highest cost. A multi-family office serves several client families, sharing operational costs while still delivering professional wealth management and advisory services.

How do family offices invest differently from private banks?

Family offices increasingly favour direct investment in private markets, including real estate, private equity, and venture capital, rather than relying on publicly listed funds. This approach gives families greater control and often better alignment with long-term legacy goals.

Why do so few family offices have succession plans?

Despite the clear need, only 35% of family offices have a formal succession plan. The most common reason is that families delay difficult conversations about wealth transfer until a crisis forces the issue, by which point options are limited and costs are high.