- Bespoke wealth management offers fully personalized financial services tailored to an individual’s unique goals, behavior, and circumstances. It provides direct asset ownership, comprehensive estate and tax planning, and integrates behavioral insights to reduce impulsive decisions and enhance long-term outcomes. The service’s cost reflects its complexity, with provider selection emphasizing trust, behavioral assessment capability, and breadth of expertise over simple fee comparisons.

Bespoke wealth management is defined as a fully customised financial service built around an individual’s specific objectives, behaviour, and circumstances rather than a generic template. Unlike standard wealth management, it treats high-net-worth individuals and families as distinct clients with distinct needs, not as segments in a model portfolio. The service typically spans personalised financial planning, customised investment strategies, estate structuring, tax optimisation, and wealth protection. Firms such as Dimensional Fund Advisors have demonstrated that portfolios designed around individual tax positions and ethical preferences consistently outperform one-size-fits-all solutions. Tools like the MoneySign® behavioural assessment go further, mapping a client’s financial personality before a single asset is allocated. The result is a plan that reflects who you are, not just what you own.

What is bespoke wealth management vs standard wealth management?

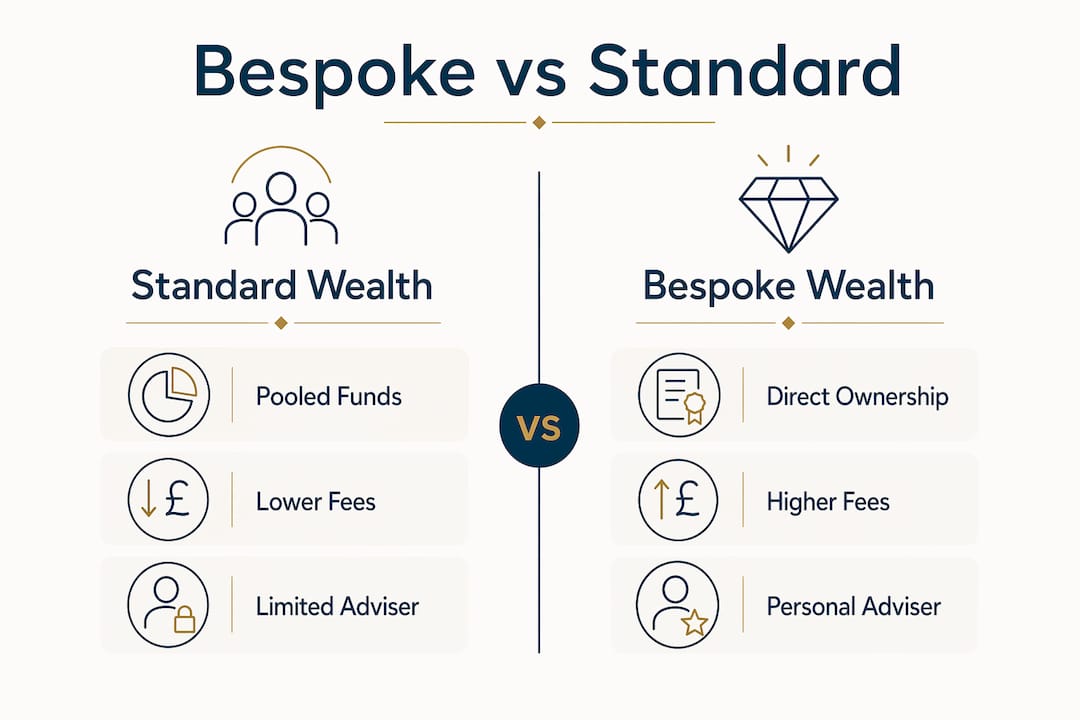

The core distinction between bespoke and standard wealth management lies in asset ownership and adviser involvement. Standard wealth management places client funds into model portfolios, pooled vehicles where every investor holds the same underlying assets in the same proportions. Bespoke investment management gives you direct ownership of assets, which means your portfolio can exclude specific stocks for ethical reasons, harvest tax losses on individual positions, and adjust allocations without triggering unnecessary capital gains across the entire fund.

The practical implications are significant. A client with a substantial holding in a single employer stock, for example, needs a portfolio built around that concentration risk. A model portfolio cannot accommodate that. Bespoke advice can, and it does so with the kind of adviser discretion and governance that balances structure with genuine personalisation.

Cost structures differ too. Model portfolios typically charge lower annual fees because the same portfolio serves hundreds of clients simultaneously. Bespoke services charge more because the work is genuinely individual. That cost difference is not a premium for its own sake. It reflects the complexity of managing a portfolio built specifically for your tax position, your estate structure, and your investment preferences.

| Feature | Model Portfolio | Bespoke Wealth Management |

|---|---|---|

| Asset ownership | Pooled fund units | Direct ownership of individual assets |

| Tax-loss harvesting | Not possible at individual level | Available on specific positions |

| Ethical exclusions | Limited or none | Fully accommodated |

| Adviser involvement | Low to moderate | High, ongoing, and personalised |

| Cost | Lower annual fee | Higher fee reflecting complexity |

| Portfolio transitions | Immediate, no tax planning | Gradual implementation to manage capital gains |

Pro Tip: When evaluating a wealth manager, ask directly whether they operate on a discretionary or advisory basis. Discretionary managers act without seeking approval for every trade, which is essential for timely tax management. If they cannot answer clearly, that tells you something important about their process.

How does behavioural financial planning shape bespoke wealth?

Truly personalised financial plans are built around client financial behaviour, not just risk questionnaires. Standard wealth management categorises clients as cautious, balanced, or adventurous and assigns a corresponding model. That approach ignores the reality that two clients with identical risk scores can behave entirely differently when markets fall 20% in a month.

Behavioural tools like MoneySign® assess how a client makes financial decisions, what emotional triggers lead to impulsive choices, and how they respond to uncertainty. That information shapes the portfolio construction, the communication frequency, and the type of assets included. A client who historically sells during volatility benefits from a more defensive allocation and a pre-agreed protocol for market downturns. A client who tends to chase performance needs guardrails built into the plan itself.

The benefit is measurable. Plans aligned with client behaviour reduce panic selling and impulsive decision-making, which are among the most damaging forces on long-term returns. Staying invested through a correction is worth more than most tactical allocation decisions.

Here is how behavioural traits translate into practical plan adaptations:

- High anxiety during volatility: Larger allocation to income-generating assets, more frequent adviser check-ins, and a written drawdown protocol agreed in advance.

- Overconfidence in concentrated positions: Structured diversification schedule with clear milestones, removing the decision from the emotional moment.

- Impulsive decision-making: Cooling-off periods built into the investment policy statement before any significant portfolio change is executed.

- Loss aversion: Portfolio framing focused on income and capital preservation rather than total return benchmarks.

- Long-term orientation: Greater allocation to illiquid alternatives such as private equity or infrastructure, where patience is rewarded.

Pro Tip: Ask any prospective adviser how they assess your financial personality before they recommend a portfolio. If the answer is a standard risk questionnaire with five questions, the plan they build will be standard too.

What services does bespoke wealth management include?

Bespoke wealth management covers far more than investment selection. Comprehensive tailored wealth services span tax optimisation, estate planning, risk management, charitable giving, and complex asset management. For high-net-worth families, the scope extends to multigenerational wealth transfer, family governance structures, and the management of assets that do not sit neatly in a brokerage account.

Estate planning within a bespoke service addresses the specific structure of your assets, your family composition, and your jurisdictional exposure. For clients with assets or beneficiaries across multiple countries, cross-border tax structuring and international estate considerations are not optional extras. They are central to the plan. Standard financial planning rarely touches this level of complexity.

Alternative assets present another area where bespoke management adds clear value. Fine art, classic cars, watches, aviation assets, and collectibles require specialist valuation, insurance, and succession planning. These assets are illiquid, emotionally significant, and often underrepresented in a client’s formal financial picture. A genuinely bespoke service accounts for them.

| Service Area | What It Covers | Client Benefit |

|---|---|---|

| Investment management | Tax-aware portfolio construction and ongoing rebalancing | Returns aligned with personal tax position and goals |

| Estate planning | Wills, trusts, and multigenerational transfer structures | Wealth preserved across generations with minimal tax leakage |

| Cross-border tax | International structuring for clients with multinational assets | Compliance and efficiency across jurisdictions |

| Wealth protection | Insurance, risk management, and liability planning | Assets protected against unforeseen events |

| Alternative assets | Fine art, watches, aviation, collectibles | Full picture of net worth with specialist oversight |

| Charitable giving | Donor-advised funds, philanthropic structures | Tax-efficient giving aligned with personal values |

Nxdfamilyoffice takes this breadth seriously. Their tax advisory services and lifestyle assets advisory sit alongside core wealth management, reflecting the reality that high-net-worth life does not separate neatly into financial and non-financial categories.

What does bespoke wealth management cost, and how do you choose a provider?

Bespoke wealth management fees reflect the depth of service provided. Typical costs include a one-time financial planning fee of approximately £2,500–£3,000 and ongoing management fees of around £3,000–£4,000 annually or roughly 1% of assets under management. The exact figure depends on portfolio complexity, the number of jurisdictions involved, and the breadth of services required.

Those fees are justified by adviser involvement and the complexity of genuine customisation. A client with a £5 million portfolio, property in two countries, a family trust, and a collection of classic cars requires a fundamentally different level of work than a client with a single ISA and a pension. The fee reflects that difference.

Choosing the right provider requires more than comparing fee schedules. Consider these criteria:

- Fiduciary commitment: Does the adviser act solely in your interest, with no referral fees or product commissions distorting their recommendations?

- Behavioural insight capability: Can they demonstrate how they assess and accommodate your financial personality, not just your risk tolerance?

- Service breadth: Do they cover estate planning, tax structuring, and alternative assets, or do they focus narrowly on investment management?

- Transparency: Are fees disclosed clearly, including any third-party charges on underlying investments?

- Track record with similar clients: Can they provide references or case studies from clients with comparable complexity?

- Communication style: Do they proactively contact you, or do you chase them? The answer matters more than most people realise.

Pro Tip: Calculate the total cost of your current arrangement, including platform fees, fund charges, and adviser fees. Many clients paying 0.5% for a model portfolio are actually paying 1.5% or more once all layers are included. A bespoke service at 1% of assets under management may cost less in total.

Key takeaways

Bespoke wealth management delivers superior outcomes for high-net-worth clients because it aligns investment strategy, tax planning, and behavioural insight with each client’s specific circumstances rather than a generic model.

| Point | Details |

|---|---|

| Direct asset ownership | Bespoke portfolios give you individual holdings, enabling tax-loss harvesting and ethical exclusions unavailable in pooled funds. |

| Behavioural alignment | Plans built around your financial personality reduce panic selling and improve long-term adherence to strategy. |

| Comprehensive service scope | True bespoke management covers estate planning, cross-border tax, alternative assets, and wealth protection, not investment alone. |

| Fee transparency matters | Ongoing fees of around 1% of assets under management are justified when the service covers genuine complexity and full adviser involvement. |

| Provider selection criteria | Prioritise fiduciary commitment, behavioural insight capability, and service breadth over headline fee comparisons. |

Why behavioural fit matters more than most clients realise

I have worked with clients who arrived with technically sound portfolios and still made costly mistakes. The portfolios were well-constructed. The problem was that nobody had ever asked how those clients actually behaved under pressure.

One client, a successful entrepreneur with a seven-figure portfolio, had a written investment policy that called for a 60% equity allocation. When markets fell sharply, he sold everything and moved to cash. His adviser had never assessed his emotional response to loss. The plan was right on paper. It was wrong for the person holding it.

That experience shaped how I think about bespoke wealth management. The investment strategy is almost secondary to the behavioural framework around it. A client who understands their own triggers, and has a plan that accommodates them, will outperform a client with a theoretically superior portfolio who abandons it at the worst moment.

The other shift I have observed is in complexity. High-net-worth clients today are more likely to have assets across multiple jurisdictions, business interests at various stages, and family structures that do not fit standard templates. The advisers who serve them well are the ones who treat that complexity as the starting point, not an afterthought.

Trust is the foundation of all of this. Not trust in the abstract, but trust built through transparency, consistent communication, and advice that is visibly free from conflicts of interest. When an adviser has no financial incentive to recommend one product over another, the quality of the conversation changes entirely. That is the standard every bespoke client should demand.

How NXD Family Office delivers tailored wealth services

Nxdfamilyoffice was built on a straightforward principle: clients deserve advice that is genuinely theirs, not shaped by referral fees or product commissions. For high-net-worth individuals and families, that means access to a curated network of expert advisers across financial planning, private banking, tax structuring, and lifestyle asset management, all coordinated without conflicts of interest.

Beyond the financial, Nxdfamilyoffice manages the full picture. From venture capital advisory to classic cars, aviation assets, and experiences that money alone cannot arrange, the service reflects how high-net-worth life actually works. If you are ready to work with advisers who put your interests first, explore Nxdfamilyoffice’s bespoke wealth management services and request a consultation.

FAQ

What is bespoke wealth management in simple terms?

Bespoke wealth management is a personalised financial service built entirely around your specific goals, tax position, behaviour, and assets. It differs from standard wealth management by providing direct asset ownership and individual planning rather than placing you into a shared model portfolio.

Who qualifies for bespoke wealth management?

High-net-worth individuals with at least £1 million in investable assets typically qualify, with very-high-net-worth clients at £5 million and ultra-high-net-worth clients at £30 million or more. The greater the complexity of your financial situation, the more value a bespoke service delivers.

How does bespoke wealth management handle tax?

Bespoke portfolios use direct asset ownership to apply tax-loss harvesting on individual positions and manage capital gains through gradual portfolio transitions. Cross-border tax structuring is also included for clients with assets or family members in multiple jurisdictions.

What is the difference between bespoke and discretionary wealth management?

Bespoke refers to the level of personalisation in the plan and portfolio construction. Discretionary refers to the authority the adviser holds to make investment decisions without seeking your approval for each trade. Many bespoke services operate on a discretionary basis, combining personalised strategy with timely execution.

How do i know if my current wealth manager is truly bespoke?

Ask whether you own the underlying assets directly or hold units in a shared fund. Ask how your financial behaviour was assessed before the portfolio was constructed. If the answers point to model portfolios and a standard risk questionnaire, the service is not genuinely bespoke.